Building a Greener Future: Insights on Green Cities and Sustainable Development – An Interview with Roni Kvatchadze 17 Apr 2024

Non-Timber Forest Product (NTFP) Value Chain Analysis in Guria, Mtskheta-Mtianeti, and Kakheti 2 Apr 2024

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 21: Ukraine’s Monetary Stability: Monetary and Exchange Rate Policy 5 Dec 2023

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 20: Ukraine: Reconstructing International Trade 5 Jul 2023

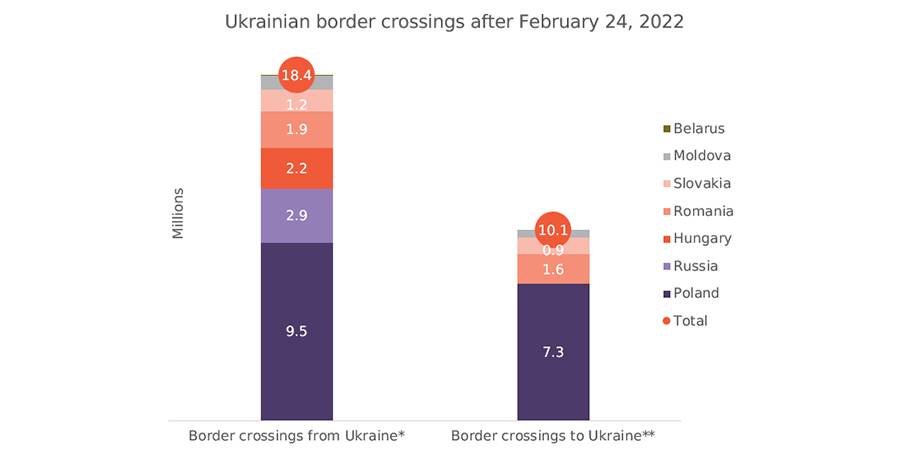

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 19: Ukrainian Refugees and their Effect on Labor Markets at Home and Abroad 2 Mar 2023

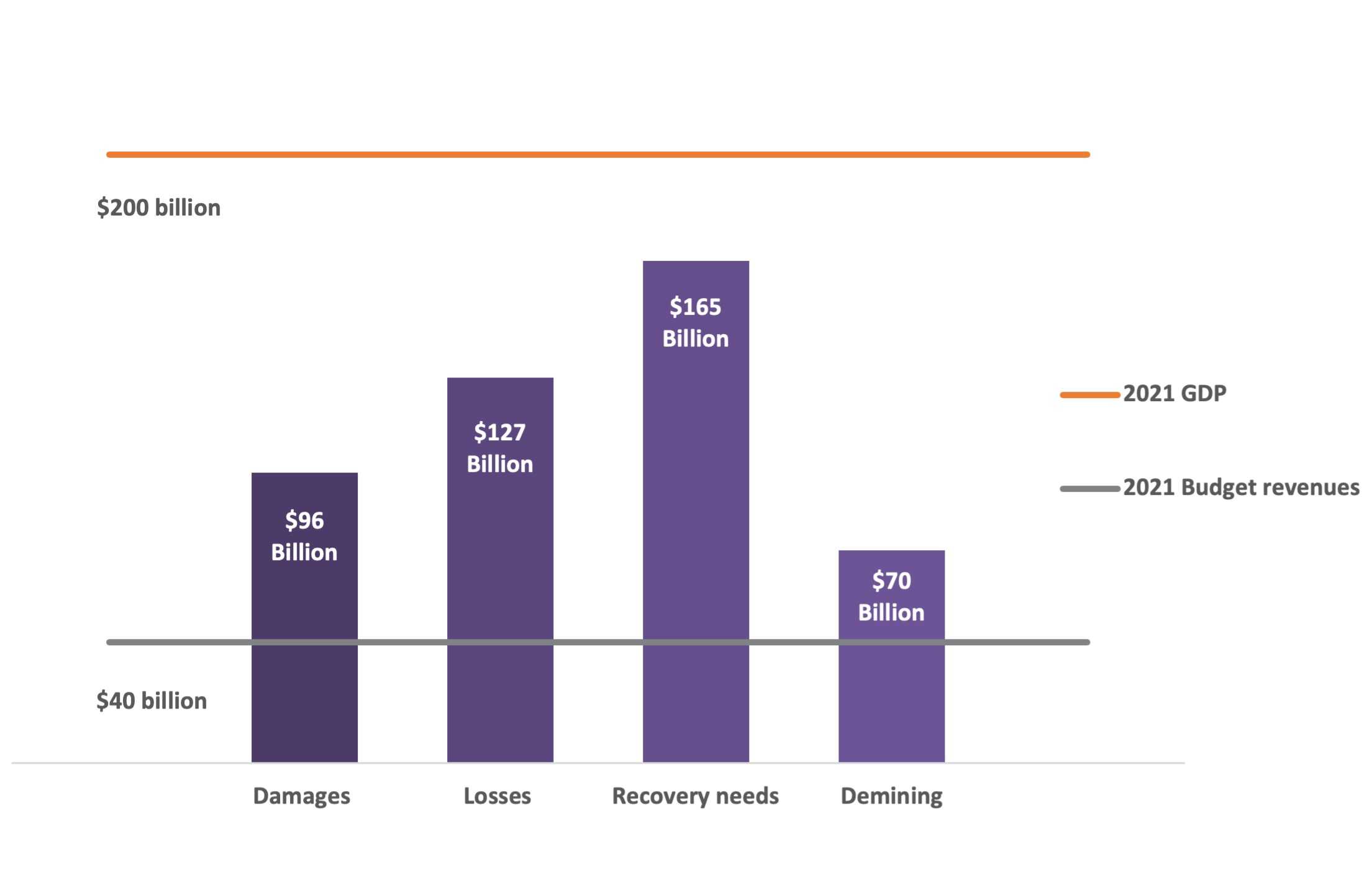

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 18: Audit of War Damage and Overview of Ukraine’s Budget for 2023 9 Jan 2023

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 17: Ukraine’s Maritime Trade and Port Infrastructure 1 Dec 2022

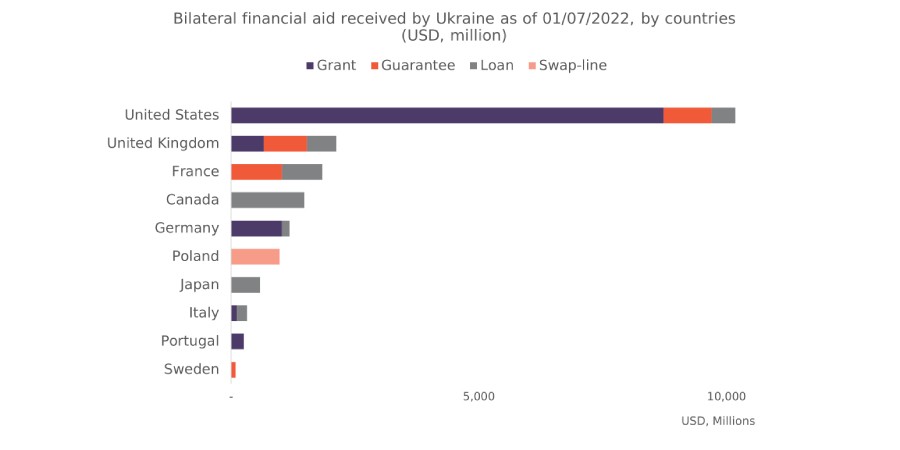

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Overview of the Measures Taken to Support the Ukrainian Economy During the War 18 Aug 2022

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Special Issue: Assessment of the Effectiveness of Sanctions Against Russia 6 Apr 2022

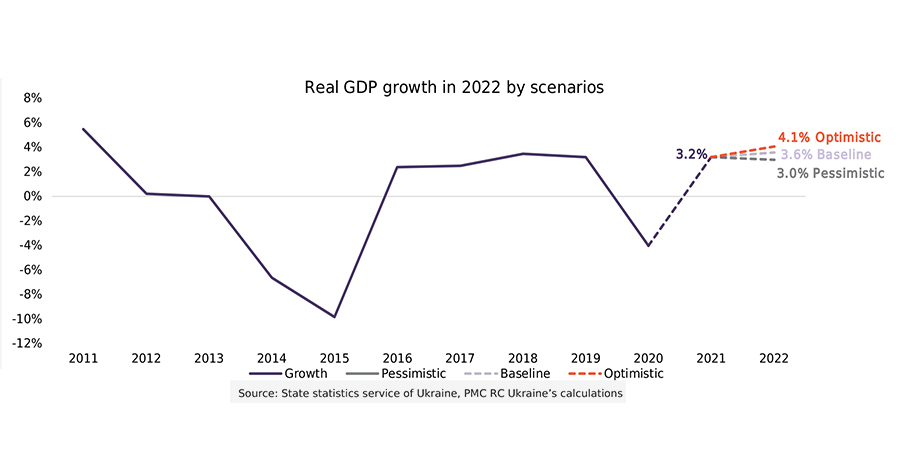

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 14: Economic Growth Forecasts in Ukraine: 2022 14 Jan 2022

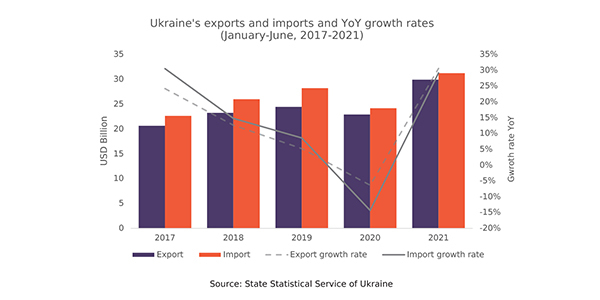

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 12: Ukraine’s External Trade (January-June, 2017-2021) 4 Oct 2021

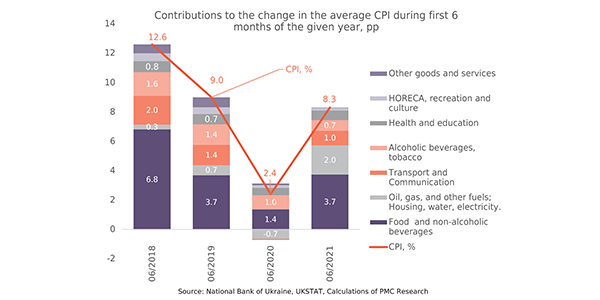

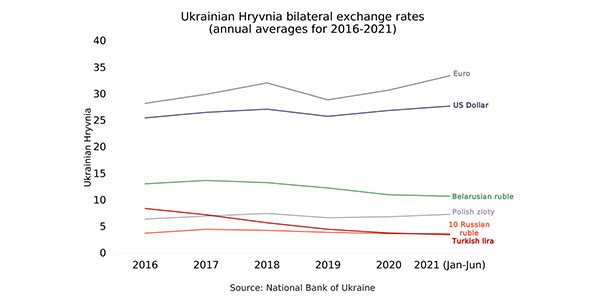

ECONOMIC OUTLOOK AND INDICATORS IN UKRAINE Issue 10: Exchange Rates in Ukraine (2016-2021) 12 Aug 2021